BTC/Crypto Nuclear Armageddon

Perhaps not - there's a Glimmer of Hopium.

Normally when the markets start nose-diving, I disconnect. That means touching grass—maybe it's 4x4'ing through mountain switchbacks, hitting a lion cub café with the kids, or heading out sailing when it’s looking particularly grim. Nature > screens when volatility's got everyone panicking.

That said, for those of us who’ve been tracking the Israel-Iran situation—long before headlines picked it up—it was always clear it would reach a boiling point. And here’s the thing: Iran, like North Korea, like Pakistan, and to some extent Russia—these aren’t just rogue actors. They’re chess pieces. Proxies in a much larger geopolitical game where China is setting the board. Iran’s proxies (Houthis, Hezbollah, Hamas) are extensions of this; Russia’s got its own (Belarus, some 'Stans), while North Korea remains oddly standalone, a wildcard.

This recent escalation needed to happen. As a Jew, sure, it hits personally. But strategically, it was about regional and global balance. The U.S. played it masterfully. I’ve got ears across some useful airwaves—was handy during the Russia-Ukraine spike, and again when India-Pakistan were squaring off. This time? Same signals: fuel movements, plane logistics, chatter increasing. The timing? Over a weekend, of course—cleaner market impact when exchanges are closed. A delay would've been messy. Trump once said he'd wait 20 days to act—narrative control. But this? Surgical.

So when I got the 4AM ping from an RRAF Aussie mate—it was go-time. Iranian social media was eerily quiet, then boom: info tsunami. Back to bed, woke up, messaged the another ex-Aviation guy (knew he’d appreciate the nuance), then went about my day. Markets were already buckling, and when things are this volatile, sometimes you don’t trade—because if you believe in the Global Liquidity Refi Cycle, you know that volatility is noise. The signal? Liquidity always returns. It’s inevitable...unless, of course, the world ends.

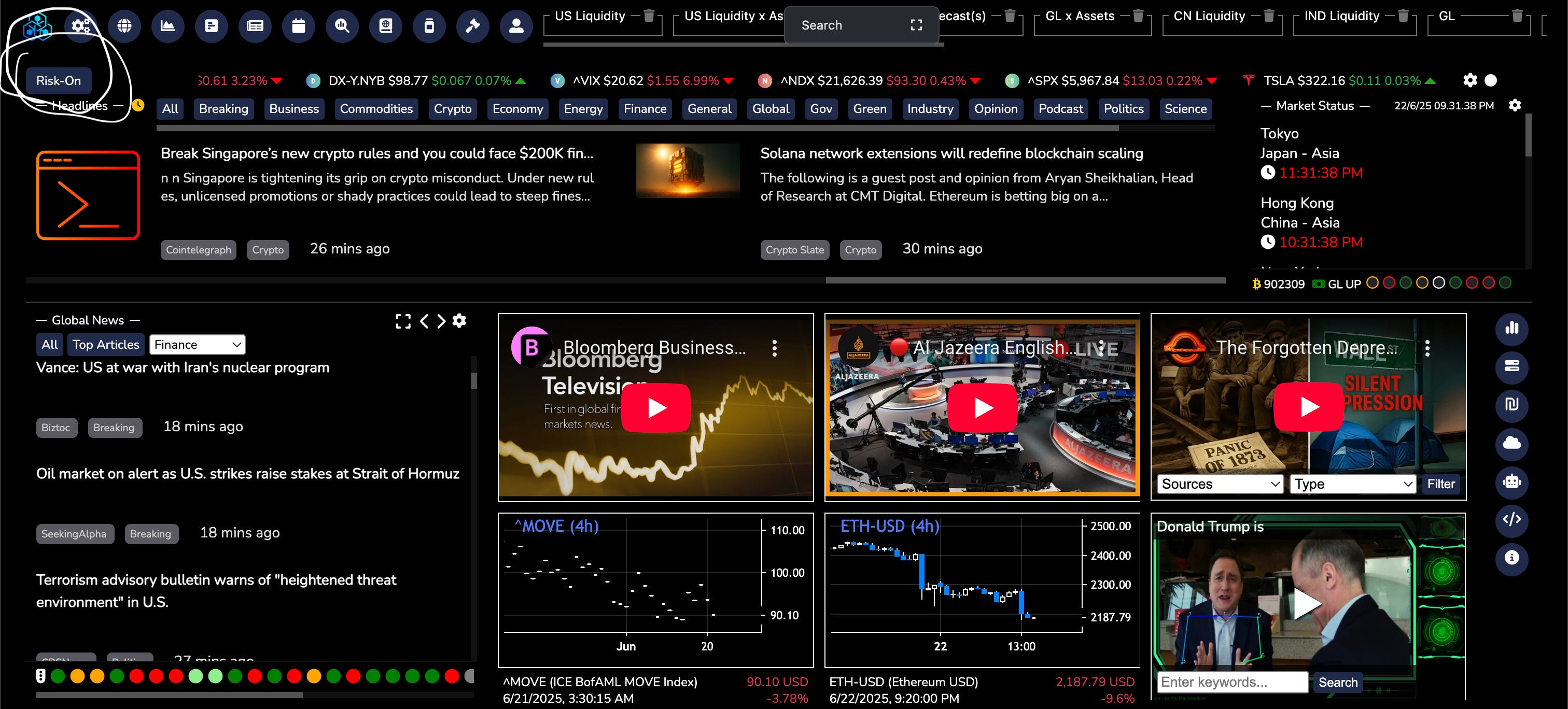

Later that evening, after dunking on a few Chinese Twitter bros over their Strait of Hormuz takes (yes, 90% of Iran’s oil exports go through it, and yes, that mostly feeds China), I jumped back into my Terminal. And there it was: top left corner flashing... Risk-On.

That caught me off guard.

The BTC-SMB impact chart had already flagged downside below $100k weeks ago—13-week lag from liquidity shifts. Most systems were flashing caution. Momentum changes, credit tightness, geopolitical overhang... all pointing to "brace". So what was I missing?

For Some Context — Some of the Algo(s) for Quick Scanning Daily

Some More:

Interest piqued.

I flipped over to our crypto macro dashboards. We've got 2,000+ dynamic charts running on backend ANI logic—slicing data every which way. No manual bias. Raw signal.

Zooming out, we’re in what the system has ca Macro Spring.

US: Macro Fall (tariff instability)

Asia: Macro Winter (liquidity exodus, largely due to US pressure)

Europe: Macro Summer (military spending ramping up)

FYI: shitcoins usually don’t run until Macro Summer/Fall. Spring is Financial Conditions preloading—the warm-up phase. That’s why alts are dead right now. The business cycle has been a flaming garbage heap, and while there’s some liquidity sloshing around, it’s either misallocated or still timid. 2021 PTSD is real. But remember: Central Banks inject monetary inflation. Variable inflation? That’s downstream. That only kicked in when normies got paid. So, yeah, follow the liquidity. Don’t chase GDP logic—GDP’s a lagging narrative used to justify political grift.

Now to Bitcoin.

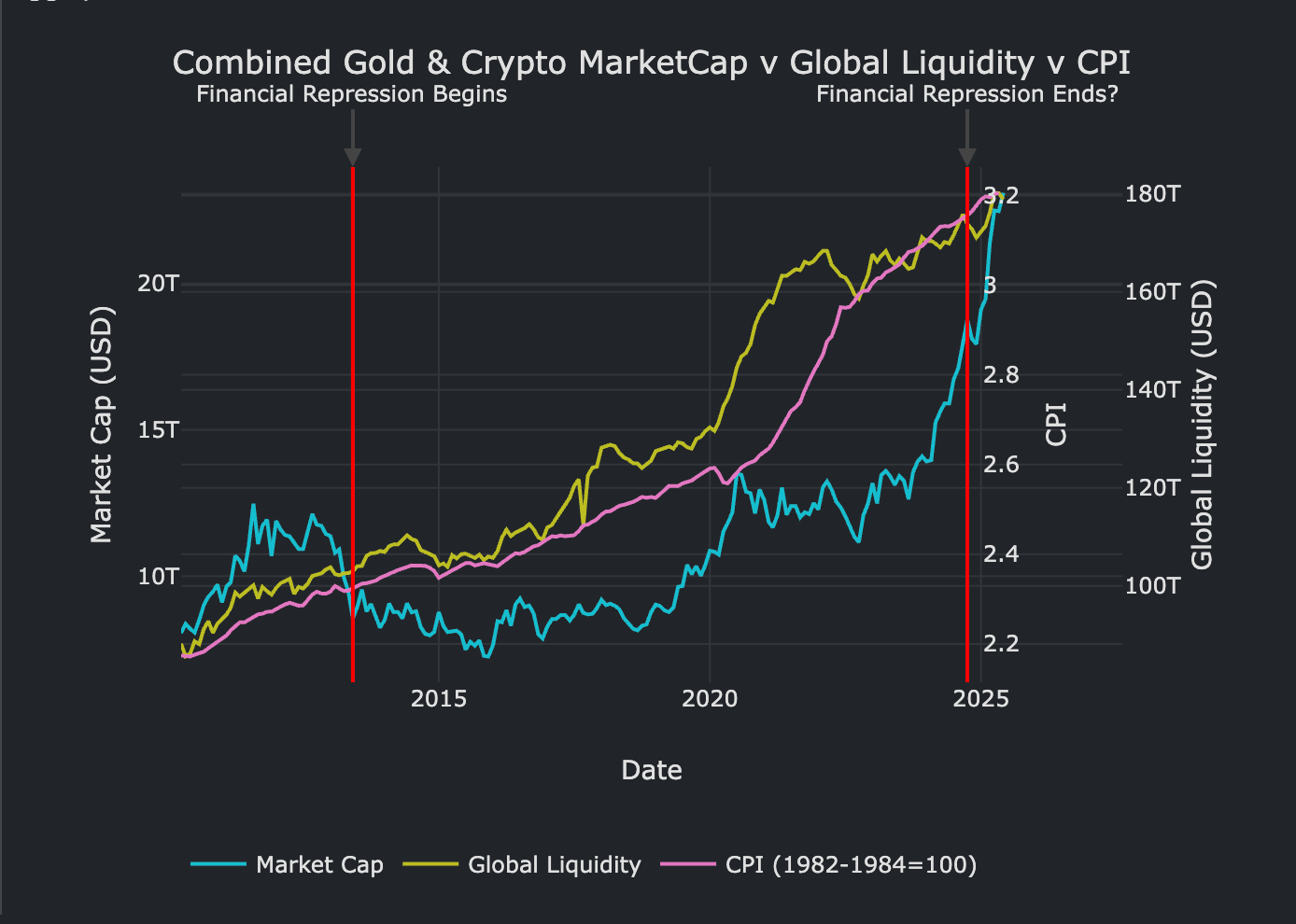

BTC is a macro asset. It’s tech + fixed supply = reacts to global liquidity like clockwork. Liquidity spikes → speculation kicks in → BTC flies. That’s the downstream chain: Liquidity → Financial Conditions → Business Cycle → Speculative Mania.

BTC is the beneficiary of this process. And also the canary.

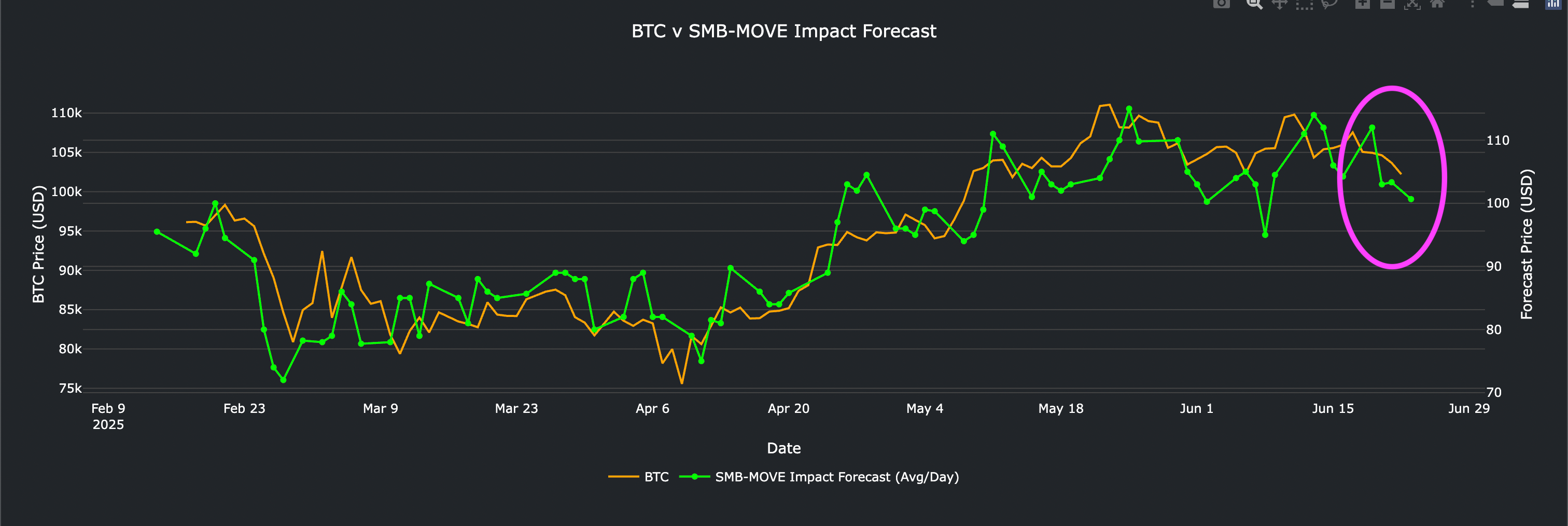

Some say BTC tracks Global M2. Sure, kinda. But that’s not tight enough. You want Total Global Liquidity (TGL)—and better yet short-term slice and dice for the the Shadow Monetary Base (SMB). That’s Eurodollar credit, hypothecation flows, real-world collateral dynamics. BTC lags TGL by ~8–12 weeks. So our chart shows BTC vs. TGLI 13m Change (smoothed)—not pretty right now. But TGLI (inverted) still trending up = cycle’s still alive.

In the above chart you have PBoC Total Assets YoY shifted forward 4 Months which provides a good insight into some respects the price direction of BTC, it should be noted they’ve just injected capital into their markets today.

Rather than giving individual charts, as although they paint a picture they don’t paint the picture itself.

Now aside from the following.

Financial Conditions Index (FCI)? Still easing. The U.S. one (NFCI) might look tight, but globally it’s a green light. Europe offsets the Fed’s foot-dragging.

BTC breaking from Term Premia? Interesting. Historically happens at peaks or troughs. This one looks like a peak formation—projecting $70k. But here’s the mismatch: macro isn't peaking. Financial conditions still loosening, business cycle still flaccid. Doesn’t add up.

BTC 28d Change / ARK 20d Change diverged. ARK still tracks ISM. So BTC divergence = not U.S.-led. My take? It’s Eurodollar-credit related (again: SMB). Global liquidity nuance.

The Nowcast for economic momentum says we’re in early recovery. That’s bullish. Risk (inverted) also up = risk appetite returning.

Dollar’s tanking. Trump jawboning the Fed. Shadow Monetary easing quietly continues. But Treasury’s gone limp on YCC (yield curve control). BTC broke away from this recently. Bessent says they’ll stick to it (no choice), but it’s barely QE. Liquidity’s still constrained.

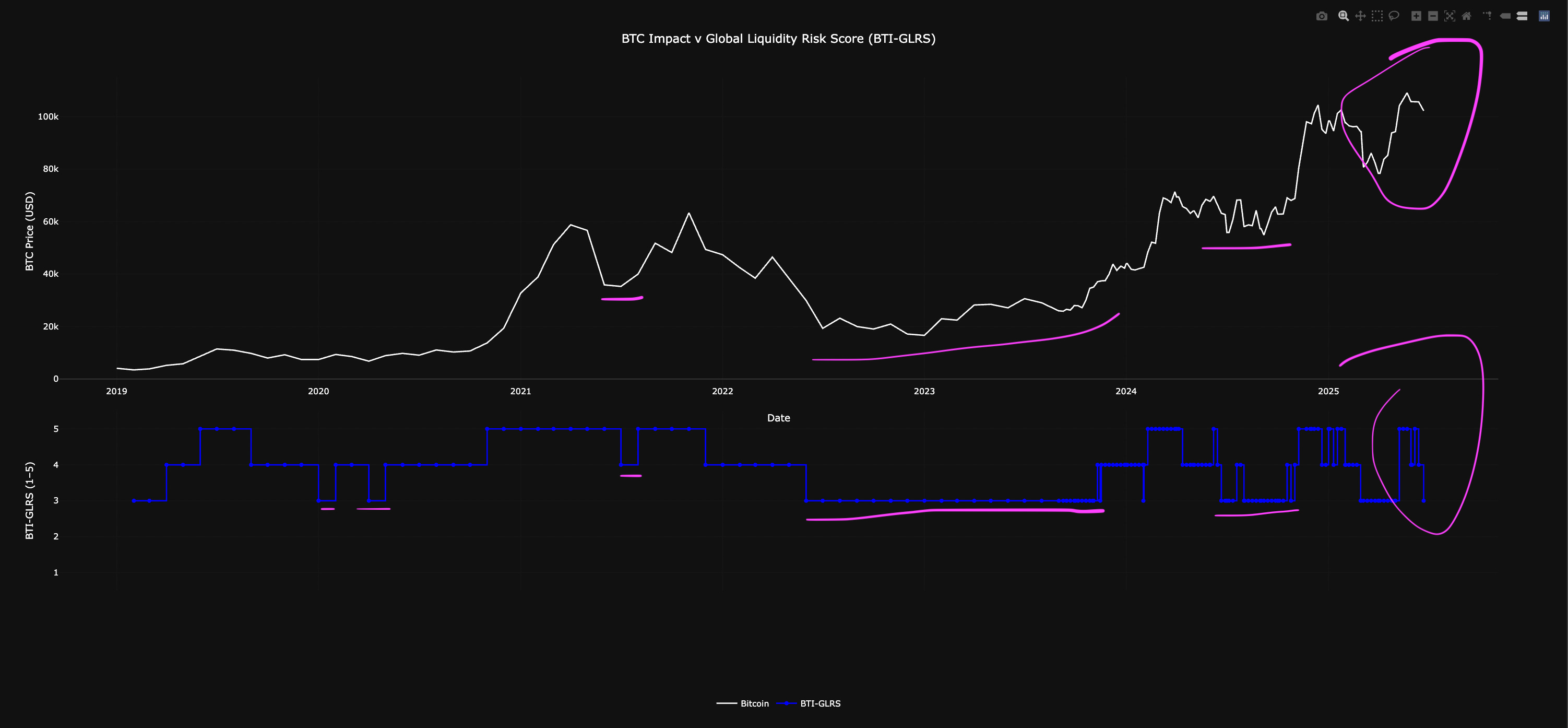

BTC has now tagged the upper band of Total Global Liquidity twice. That’s not price resistance—it’s macro resistance. There’s simply not enough liquidity in the system. If Global Liquidity (upstream) doesn't rise significantly, Financial Conditions (midstream) can’t loosen further, and GDP (downstream) can’t catch up. No GDP = no debt rollover = instability.

And finally, the carry trade.

Oil up = Japan pain = Yen weakens as they chase crude. Weak Yen tightens the Yen$ carry. That hurts Eurodollar credit. That stiffs TGL. Markets feel it.

Add to that:

PBoC liquidity injections (spotted it, massive)

Stablecoin velocity exploding

USD velocity still rolling over

Liquidity-to-debt ratios weakening

So where are we?

I’m chalking this Risk-On burst up to:

Easing Financial Conditions

Geopolitical shock priced in

Tariff chatter = noise

Even though plenty of signals flash caution, the system’s logic seems to be: "This is the moment for risk."

It’s insane.

But then again, everything’s insane when liquidity is the only thing keeping the game alive.

"Markets climb walls of worry—but liquidity builds the damn stairs."

And that’s where we are.

— Bro'd out, logged in, best approach — watching it all from the beach in Asia.