Yen Carry Trade Unwinding: Is the UK (GBP) About to Pick Up the Slack?

This isn’t a return to empire — it’s a return to relevance. The UK has stepped forward not with an army, but with balance sheet firepower.

The unwinding of the Japanese Yen carry trade marks not just the end of a financial era but the opening of a geopolitical and monetary reshuffling. As Japan signals its structural exit from serving as a Dollar liquidity conduit, the United Kingdom — with its deep Eurodollar roots and offshore financial architecture — appears poised to step into the void. But this transition isn’t just about finance. It intertwines with debt diplomacy, strategic assets like the Chagos Archipelago, and quiet alignments between the US and UK in preparation for a multipolar world.

Japan's Structural Exit from the Carry Trade

For decades, the Japanese Yen served as the global funding currency of choice. With ultra-low interest rates and abundant central bank liquidity from the Bank of Japan (BoJ), global investors borrowed cheaply in Yen to invest in higher-yielding assets abroad — a practice known as the "Yen carry trade."

However, Japan can no longer afford this role, structurally or demographically:

Aging Population: Japan’s rapidly aging population is driving capital repatriation, reversing decades of persistent capital outflows. Domestic institutions now prefer to hold JGBs over riskier foreign bonds, especially as FX-hedging costs soar and liability-matching becomes urgent..

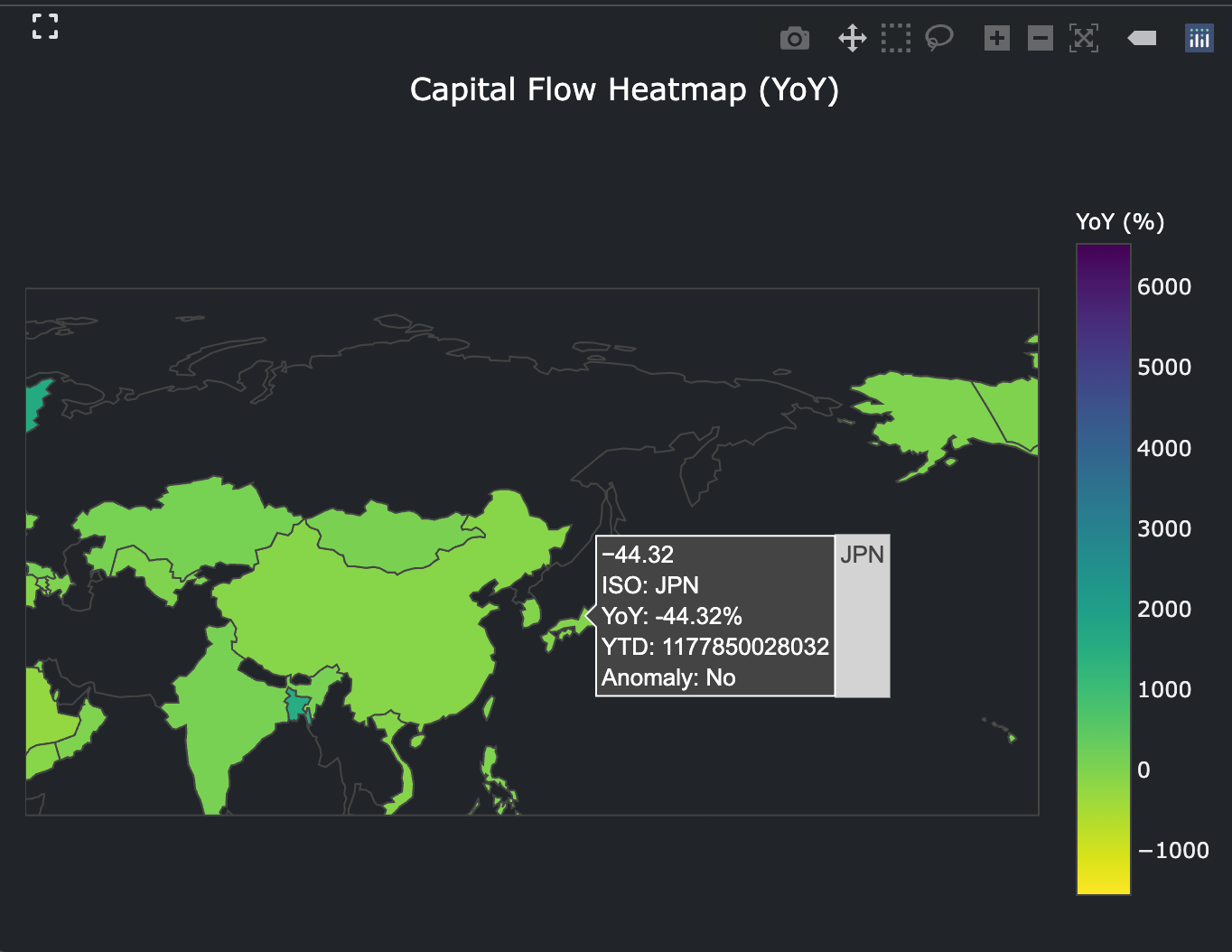

Capital Flow YoY (2025) -44.32% → Currently non-abnormal BoJ Balance Sheet Bloat: The BoJ now owns more than 50%+ of the Japanese Government Bond (JGB) market, a distortion that signals the limits of financial repression.

Currency Volatility: The weakening Yen threatens import-driven inflation in a country that imports over 90% of its energy needs.

US Pressure: Washington is less tolerant of weak-Yen policy as it exacerbates trade imbalances and fuels anti-China sentiment by proxy (as a weaker Yen indirectly helps China via regional trade).

Yen Rising - Crushing US Stocks (Nasdaq example).

How the Yen Carry Benefited China – and Why It's Being Targeted

China was a major indirect beneficiary of the Yen carry regime:

Capital Inflows: Japanese capital funneled through Hong Kong and regional hubs supported Chinese equity and real estate bubbles.

Commodities and Infrastructure: The Yen carry helped fund China’s Belt and Road Initiative (BRI) indirectly by suppressing Dollar funding costs.

Dollar Debt Expansion: Chinese corporates accumulated over $2 trillion in USD-denominated debt, much of it recycled through Eurodollar markets and offshore hubs like the Caymans and Luxembourg.

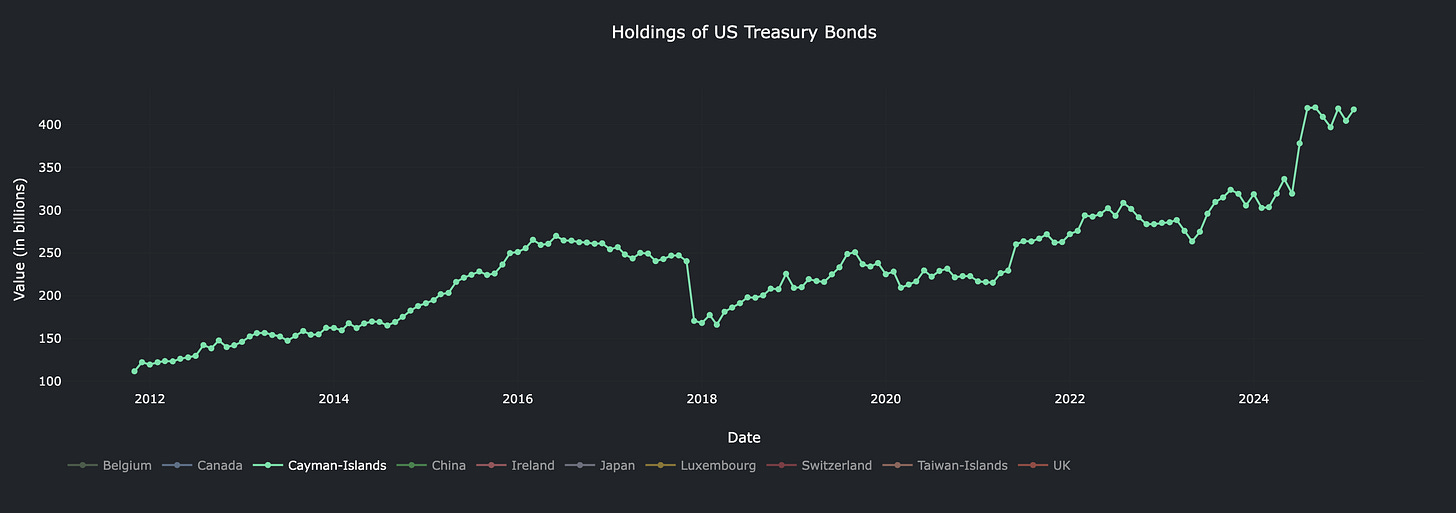

Caymans — Up by 110% Since 2020

Luxembourg — Up by 75% Since 2020.

Now, the U.S. is weaponizing Dollar access — cutting off SWIFT links, restricting CNH liquidity, and tightening repo channels — to contain Chinese expansion. China's rising attempts to cause mischief in the U.S. Treasury market (e.g., bond dumping threats, yuan diplomacy) come precisely as the U.S. faces a $9–10 trillion debt rollover window through 2025/26.

BOE and the UK: Poised for a Comeback as Dollar Liquidity Provider

As Japan exits the carry stage, the United Kingdom — long a silent pillar of the global Eurodollar system — is maneuvering to take its place. The evidence is mounting:

The BOE’s US Debt Exposure: The Bank of England has been a buyer of U.S. Treasuries in coordination with the Federal Reserve and Treasury. Losses on these holdings are implicitly underwritten by the US, a quiet quid pro quo.

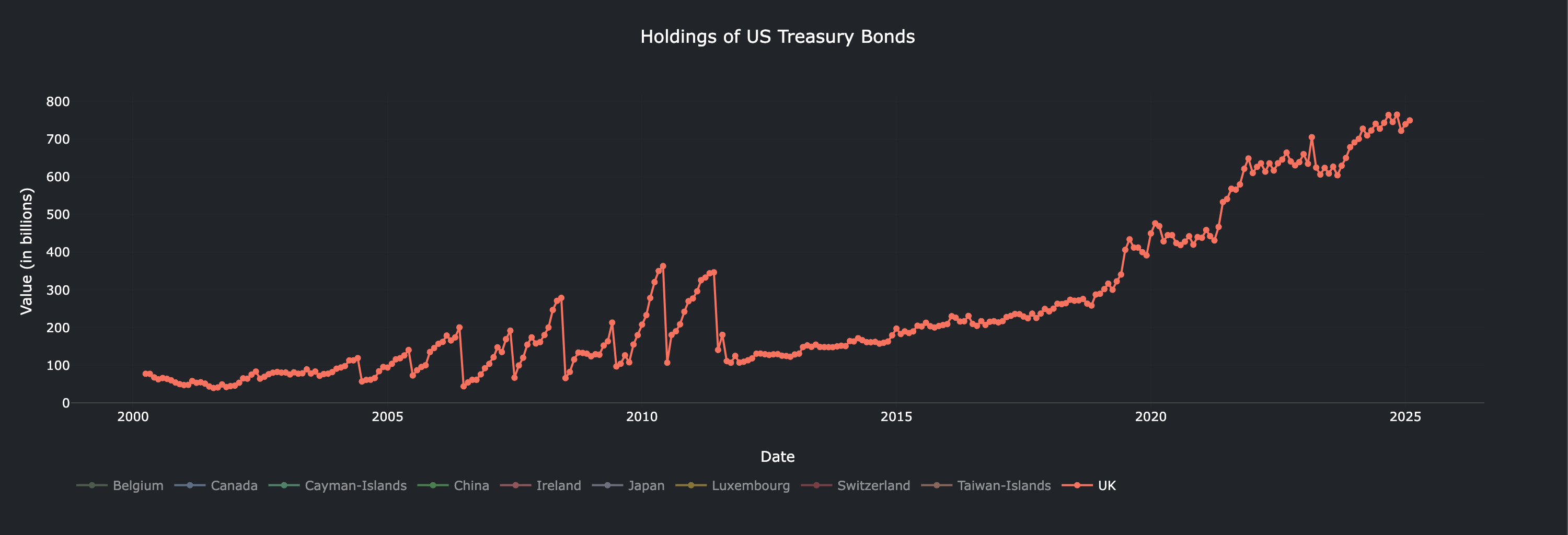

UK —Up by 100% since 2020 City of London’s Role: London remains the largest Eurodollar hub in the world, ahead of New York. BIS data shows that over 40% of all USD-based FX and interest rate derivatives pass through the City.

Offshore Dollar Ecosystem: Jurisdictions like the Cayman Islands, Gibraltar, Bermuda, Jersey, and the British Virgin Islands — all tied to the UK — serve as core nodes in the Eurodollar network, providing shadow liquidity and synthetic USD pools that operate outside Federal Reserve oversight.

Chagos Archipelago: A Strategic Bargaining Chip in the Dollar Realignment

At first glance, the United Kingdom’s recent willingness to cede the Chagos Archipelago — home to the strategic Diego Garcia U.S. military base — to Mauritius seems inexplicable. The islands never belonged to Mauritius in any sovereign capacity prior to UK administration. So why would the United States, amid intensifying great-power competition, endorse handing strategic territory to a country that maintains warm ties with China?

Source: https://www.ft.com/content/e03ab89d-42fc-44ab-89fe-7ed086f0ab3a

The answer lies in a backroom financial bargain, not a moral one.

Mauritius & China: Though nominally non-aligned, Mauritius has deepened economic ties with China under the Belt and Road framework. Handing over control of Chagos — even symbolically — would ordinarily raise red flags in the Pentagon. But Washington showed unusual openness.

UK Leverage via the Dollar System: The UK's real leverage came not from the territory itself, but from its ability to step into the vacuum left by the collapse of the Dollar/Yen carry trade — a system that for decades helped lubricate global capital markets and supported demand for U.S. Treasuries.

Trump Cornered by Liquidity Risks: With Japan pulling back from its role as a Dollar liquidity conduit, and China actively reducing exposure to U.S. Treasuries while threatening market disruption, the U.S. faced a dangerous cliff: $9–10 trillion in debt rollovers through 2026, and a shrinking pool of natural buyers.

The Bargain: The UK — uniquely placed through the City of London and its offshore financial hubs — signaled that it could help fill the liquidity gap via Sterling-based structures and institutional purchases of U.S. debt. In exchange, the U.S. would quietly approve the symbolic transfer of Chagos to Mauritius, while retaining full operational control of Diego Garcia through private defense agreements.

Corruption Concerns: Whispers in Westminster suggest the decision to offload Chagos may involve kickbacks and future private sector "consultancies" — not unlike Iraq or Brexit profiteering.

A red eyed Trump having a supportive arm touch from Kier Starmer.

This was not about legal history or colonial morality — it was about who underwrites the next era of Dollar hegemony.

Starmer, Trump, and the City-Wall Street Pact — Powered by BlackRock

With Keir Starmer now firmly into power, a significant financial and geopolitical shift is underway — not centered on trade or industrial strategy, but on monetary architecture and liquidity dominance. At the center of this pivot is a quiet but critical meeting: within Starmer’s first few months in office, he held a private audience with Larry Fink, CEO of BlackRock — arguably the most powerful man in global finance.

This meeting wasn’t symbolic. It was strategic.

Behind the scenes, the UK offered to step into the vacuum potentially to be left by Japan, whose Yen carry trade architecture is now structurally broken. With a declining currency, unsustainable hedging costs, and demographic collapse, Japan can no longer serve as the Dollar's offshore engine. Its exit risks catastrophic damage to U.S. Treasury markets, global capital flows, and Dollar liquidity.

Larry Fink — the de facto kingmaker of global capital allocation — is acutely aware of this risk. And with Starmer’s Labour government offering the UK as a replacement, the equation became brutally simple for Washington.

Trump bent the knee.

Faced with the potential implosion of the Dollar/Yen regime, Trump agreed to terms set by Starmer — including green-lighting the controversial transfer of the Chagos Islands to Mauritius. On the surface, it looked like a diplomatic concession. In reality, it was a forced trade to protect U.S. financial stability — and more importantly Western Hegemony.

UK Takes Over Carry Function: In a post-BoJ vacuum in carry trade demand could see GBP emerging as a minor carry currency, especially as the BOE remains behind the Fed in rate normalization.

GBP offers higher yields but, crucially, sits at the heart of the Eurodollar system.

The BOE's global reach, combined with London’s offshore spiderweb (Cayman, Jersey, BVI, Gibraltar …etc), makes it an ideal intermediary for global leverage and synthetic Dollar creation.

With Japan and China reducing Treasury purchases and offloading en-mass or maliciously, the UK fills the void:

Institutions linked to the BOE are already absorbing U.S. debt.

Losses incurred are quietly underwritten by the U.S. Treasury — a tacit guarantee to maintain GBP stability and UK cooperation.

The UK now effectively serves as a shadow Federal Reserve node, facilitating offshore Dollar liquidity flows with Washington’s full knowledge.

Trump’s Transactional Concession in return for:

Liquidity support via City of London and Eurodollar conduits,

BOE’s quiet role in stabilizing U.S. bond markets,

Ongoing alignment on military fronts (AUKUS, Diego Garcia, NATO optics),

The Trump team:

Signed off on the Chagos transfer, despite historical and strategic objections.

Agreed to provide covert support for the BOE’s U.S. asset exposure.

Signaled that GBP would remain a legitimate Dollar-proxy carry trade currency, unlocking new financial engineering capacity out of London.

The Bigger Picture: Financial Hegemony in Flux

We are witnessing a generational shift in how global liquidity is sourced, priced, and weaponized:

From Yen to GBP: The carry trade function — IF previously held by Japan — may pivot to a Sterling-centered system, blending Eurodollar legacy structures with new geopolitical alignments.

From Trade Flows to Debt Rolls: The battleground is no longer trade deficits — it’s the rollover of massive sovereign and corporate debt, and who supplies the liquidity to keep the system afloat.

From Silent Partners to Strategic Allies: The UK’s return to financial centrality is not just market-based. It is strategically approved, if not orchestrated, by the US in a new era of global containment and reshuffling.

The UK is subtly re-entering the global monetary fray, not as an empire of goods, but as an empire of capital. As Japan exits, and China is contained, Britain’s old infrastructure — from the City of London to its offshore satellites — may serve as the new arteries of Dollar liquidity, backed by implicit US guarantees and transactional alliances.

The Spiders Web — Britain’s Second Empire — Coming Back Online?

Whether the public sees it or not, the BOE’s shadow role is expanding. Chagos is just the price of admission.